Why are some health insurance plans much more expensive than others?

When comparing several international health insurance plans, the price differences can sometimes be surprising. Two policies may appear very similar but display completely different prices.

A hospitalization-only insurance plan (IPD) can cost two to four times less than a comprehensive health insurance plan that includes outpatient care, dental, optical, or medical evacuation coverage.

Many policyholders believe that the price of health insurance mainly depends on the hospitalization coverage limit. In reality, however, this is usually not the most decisive factor.

The cost of health insurance actually depends on several elements: how frequently benefits are used, the insured person’s risk profile, and the overall claims ratio of the insurance product.

In this article, we will examine the main factors that truly influence the price of health insurance.

1. The Difference Between Hospitalization Insurance (IPD) and Comprehensive Health Insurance

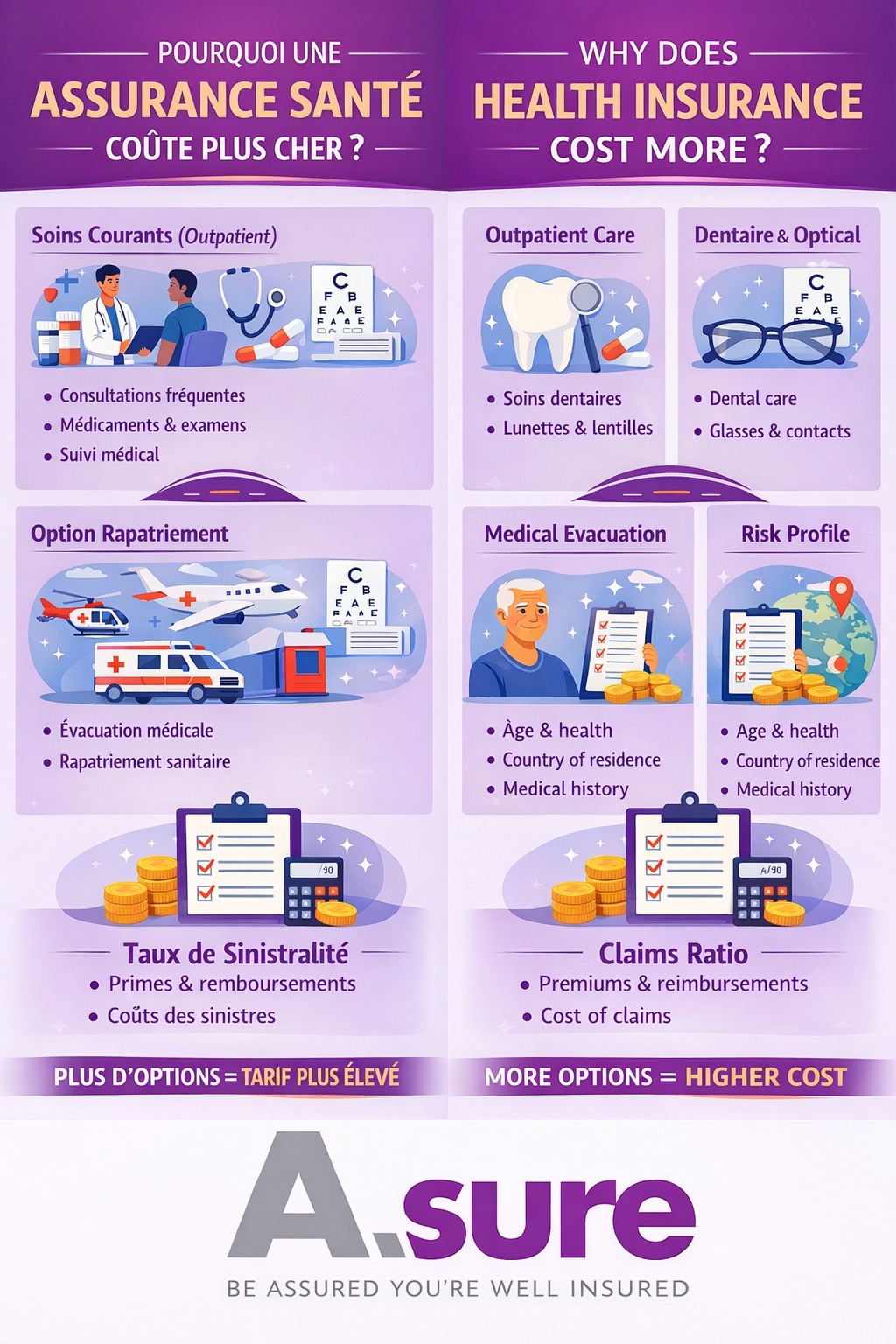

The first factor that strongly influences the price of health insurance is the level of coverage chosen.

Hospitalization Insurance (IPD)

Hospitalization insurance, often called IPD (Inpatient Only), covers only medical expenses related to hospitalization.

It generally includes:

-

surgical costs

-

hospitalization fees

-

hospital room charges

-

intensive care

-

treatments administered during the hospital stay

-

examinations required for the hospitalization

This type of insurance protects against the most expensive medical costs, which in some countries can reach tens or even hundreds of thousands of euros.

However, since hospitalizations remain relatively rare, this type of policy is usually much more affordable.

Comprehensive Health Insurance

Comprehensive health insurance includes not only hospitalization but also outpatient care.

It may cover:

-

doctor consultations

-

specialist consultations

-

medications

-

laboratory tests

-

radiological exams

-

medical follow-up

This type of coverage is more comfortable for the insured person, but it is also much more costly for insurance companies.

2. Outpatient Care: The Main Driver of Higher Costs

In most international health insurance plans, outpatient care represents the largest share of reimbursements.

Unlike hospitalization, outpatient services are used very frequently by policyholders.

They typically include:

-

medical consultations

-

specialist visits

-

medications

-

blood tests

-

medical imaging exams

-

monitoring of chronic conditions

This high frequency of use has a direct impact on the overall cost for the insurer.

Even though each reimbursement may be relatively small, their accumulation throughout the year generates a very large total volume of claims.

This is why adding outpatient coverage can double or even triple the cost of a health insurance policy.

3. Dental and Optical Benefits

Some health insurance plans also include additional benefits such as dental and optical coverage.

These benefits may include:

Dental Care

-

dental cleaning (scaling)

-

routine dental treatment

-

cavity treatment

-

dental prosthetics

-

orthodontics

Optical Care

-

glasses

-

contact lenses

-

eye exams

These benefits are often highly appreciated by policyholders, but they have a direct impact on the price of the insurance.

The reason is simple: these expenses are very predictable and very frequently used.

In a traditional insurance model, insurance is designed to cover unexpected and costly events. However, dental care or buying glasses are relatively common expenses.

As a result, including them in an insurance contract often leads to a significant increase in premiums.

4. The Medical Evacuation Option

For expatriates, international travelers, or people living in regions with limited medical infrastructure, medical evacuation coverage can be essential.

This option may include:

-

medical evacuation to a better-equipped hospital

-

medically assisted transportation

-

transfer to another country

-

repatriation to the home country

-

medical escort during transport

Although these situations remain relatively rare, they can generate extremely high costs.

A medical evacuation by specialized aircraft can easily cost tens of thousands of euros, or even more depending on the distance and the level of medical assistance required.

For this reason, insurers must incorporate this risk into the calculation of premiums.

5. The Insured Person’s Risk Profile

The price of health insurance does not depend only on the benefits chosen. It also depends on the risk profile of the insured person.

Insurance companies evaluate several criteria to estimate the probability of claims.

The main factors include:

Age

- Age is one of the most important factors.

- The older a person gets, the higher the probability of medical expenses.

- This is why health insurance premiums tend to increase progressively with age.

Health Condition

Medical history can also influence the price.

In some cases, insurers may:

-

apply a premium surcharge

-

exclude certain medical conditions

-

impose waiting periods

These measures help limit risks related to pre-existing conditions.

Country of Residence

- The cost of medical care varies significantly from one country to another.

- For example, medical costs can be particularly high in countries with predominantly private healthcare systems.

- In such regions, insurance premiums are generally higher to reflect the potential cost of treatment.

6. The Claims Ratio of the Insurance Product

Another essential factor in insurance pricing is the claims ratio.

This term refers to the relationship between:

-

the premiums collected by the insurer

-

the reimbursements paid to policyholders

If an insurance product has a high claims ratio, it means that reimbursements represent a large portion of the premiums collected.

In this case, the insurer may need to adjust the policy conditions to maintain the financial balance of the product.

These adjustments may include:

-

premium increases

-

changes to deductibles

-

reductions in certain benefits

-

restructuring of the product

7. Why Hospital Coverage Limits Have Little Impact on Price

Contrary to what many policyholders believe, the hospital coverage limit is usually not the main factor influencing the price of health insurance.

In reality, hospitalizations are events that are:

-

relatively infrequent

-

but potentially very expensive

Thanks to risk pooling, insurers can spread these costs across a large number of policyholders.

This is why increasing the hospital coverage limit of a policy usually results in only a limited increase in the premium.

By contrast, frequently used benefits such as doctor visits or medications have a much more direct impact on the price.

Conclusion

The price of health insurance depends on many factors, not only the level of hospitalization coverage.

The elements that usually have the greatest impact on the cost of a policy are:

-

outpatient care

-

dental and optical benefits

-

medical evacuation coverage

-

the insured person’s risk profile

-

the claims ratio of the insurance product

Understanding these factors makes it easier to compare the different offers available on the market and choose an insurance policy that truly matches your needs.

A good health insurance plan is not necessarily the one that offers the most benefits, but the one that provides the right balance between protection and budget.

You can also contact us to choose the right health insurance plan

Learn more about health insurance deductibles and premiums in our detailed article.

According to the 2026 Global Medical Trends Survey (WTWCO), Global medical costs are experiencing significant, sustained inflation, with projections indicating a 10.3% to 10.9% rise in 2026.

Healthcare inflation in Thailand is projected over 10% in 2026 (with some estimates suggesting up to 15% in private sectors), significantly outpacing general inflation.

0 Comments